A couple blog posts today got me thinking again about education and inequality. The first was from Economist’s View about a linking to a report by economists Heather Boushey and Carter Price at the Washington Center for Equitable Growth. In their conclusion they state:

The empirical literature has been evolving as new data become available and better

data analysis methods are applied. Initially, there was a strong body of literature

implying that economic inequality was bad for economic growth. These initial studies

had data and methodological limitations that were addressed in a second generation

of empirical papers on the subject. This second generation of papers had conflicting

results. Some found a strong negative relationship between inequality and growth,

while others found the opposite by using different approaches.

The likely source of this conflict has been identified as one of timing—studies that

look at the longer-term growth implications find that inequality adversely affects

growth rates and the duration of periods of growth, while those that focus on

short term growth find that inequality is not harmful and may be associated with

faster growth. Furthermore, studies that look at the impact of inequality on different

levels of the income distribution have found that inequality is particularly bad

for the income growth of those not at the top.

So inequality, generally speaking, is more strongly associated with negative effects in the long term than what might happen over the business cycle. We are not talking about strong evidence for a cause of secular stagnation here, though the authors of the report do mention the possibility that higher inequality might be a factor in the current slow recovery of the U.S.

The second post was from Marginal Revolution linked to a post by Josh Zumbrun entitled SAT Scores and Income Inequality: How Wealthier Kids Rank Higher. The point of that post can be summarized by this

SAT scores appear to be a monotonic function of parent income.

Alright what’s the connection here. I couldn’t help, but think about Galor and Zeira 1993 in ReStud. Their model is able to generate inequality negatively impacting growth in the long run. The basic idea is that rich kids inherit more money to go to college. However, that isn’t enough itself. If education is so beneficial to poor kids and they had access to credit, then they could get a student loan. What if that isn’t the case? In the author’s own words

This paper analyzes the role of income distribution in macroeconomics through investment in human capital. The study demonstrates, that in the face of capital market imperfections the distribution of wealth significantly affects the aggregate economic activity. Furthermore, in the presence of indivisibilities in investment in human capital, these effects are carried to the long run as well. Hence, growth is affected by the initial distribution of wealth, or more specifically by the percentage of individuals who inherit a large enough wealth to enable them to invest in human capital. Thus, we can represent our results as describing the importance of having a large middle class for the purpose of economic growth.

My guess for the importance of the indivisibilities in the investment of human capital (education) is the following. Galor and Zeira assume investment in human capital costs a fixed amount “h”. In their overlapping generation model if your parent leaves you at least “h” you get to go to school when you are young, if not you don’t. If you do go to school you get a good job when you are old and can leave your kid money to go to school. Likewise your grandkid will benefit by having funds to get education left by your child. If you start rich, your descendants will be rich.

However, if you start poor your descendants will be poor. If you don’t have money to go to school, you can’t borrow because of the credit constraints. So you will work at a low paying job when young and old. You won’t have enough money to give to your child to go to school. Also, you also can’t make incremental improvements. This is where the indivisibilities in the investment of human capital comes in. If you could just invest a little bit, you could get a slightly higher paying job, and leave a little more to your kid, who could also make an incremental improvement. There is a possibility for your descendants to catch up (at least maybe… more on this below). However, with the investment in education being all or nothing their is no incremental improvement possible.

The country is divided between rich and poor based on some initial distribution of rich and poor people. A subsidy for the poor could get around the issue of credit constraints and allow them to go to school. Everyone would be more productive and output would increase. Redistribution to the poor would increase growth. The standard equity versus efficiency trade off doesn’t apply since the subsidy is fixing a market imperfection.

Alright that is all good, but neither of the assumptions perfectly relates to what we see out in the world. However, I think that the general tenor of the assumptions are correct. With universal primary education we should obviously switch to think about higher education. First, the news media has widely publicized the increasing cost of college. That in itself wouldn’t be a concern for a rich/poor divide if the government gave large enough subsidies to poor students. But then you read studies like Hope For Whom? by Susan Dynarski, that conclude,

The federal government and the states have recently enacted a slew of new student aid programs aimed at youth from middle- and high-income families. There has been little research on the sensitivity to college costs of this group’s attendance rates. In this paper, I estimate the impact of aid on the college attendance of middle- and upper-income youth by evaluating the Georgia program that is the namesake and inspiration of the new federal Hope Scholarship: the Georgia HOPE (Helping Outstanding Pupils Educationally) Scholarship. […]

I further find that the program’s effect is concentrated among Georgia’s white students, who have experienced a 12.3 percentage point rise in their attendance rate relative to whites in comparison states. The black attendance rate in Georgia has not increased relative to that in comparison states since HOPE was introduced. The racial gap in college attendance in Georgia has therefore increased relative to its level in the rest of the Southeast. The evidence also suggests that Georgia’s program has widened the gap in college attendance between those from low-income and high-income families. The federal Hope Scholarship, which focuses on the same slice of the family income distribution as Georgia’s program, is also likely to exacerbate already large racial and income gaps in college attendance in the US.

My emphasis added. Earlier on in the paper she states

I further find that the increase is concentrated among Georgia’s white students, who have experienced a 12.3 percentage point rise in their enrollment rate relative to whites in nearby states. The black enrollment rate in Georgia appears unaffected by HOPE. The differential impact of HOPE on blacks and whites is likely due to the focus of HOPE on middle- and upper-income students who perform well in high school.

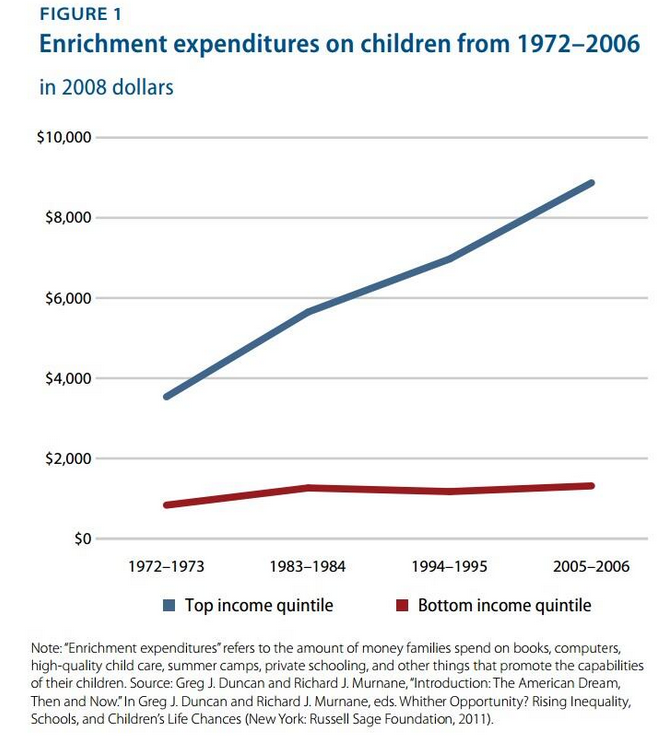

Credit constraints don’t matter so much if you can’t get into college based on high school performance. Ditto for relative performance to get into more selective colleges that might cost more. This leads me back to Josh Zumbrun’s graph above, which gives some indication of performance in high school. To give a better idea of the magnitude for last years numbers a 1324 would be between the 30-21 percentile, while a 1722 would be 75-76 percentile. Of course this would be the average of the students in the income categories and we don’t know the overall variation of scores in the categories. Plus its not controlling for other factors like parental education that might be important.

This post is getting long enough so a few extra things to think about

- Josh Zumbrun mentions in his post that test prep doesn’t explain all the variation and in fact as mentioned here minority students spend more on test prep.

- However test prep isn’t the only way the income could impact a student that would depend on student income.